Hi Aurelie, so what do you do and what brought you to Asia?

I have quite a diverse background between Tech, Finance and Start-Up creation.

From Certified IT Architect at IBM to top Investment Banks’ front office management roles, I also co-founded start-ups in Tech and Education. In investment banking roles, I have often spearheaded new teams, launched new products and pushed the bank’s digital transformation.

All of your career has been with banks, sometimes chairing their digital council: How do you see banks acting to survive the disruption from fintechs?

VC fintech investment went from $1.8 billion in 2011 to $31 billion in 2018.

Deal size in Asia are almost twice as big as the global average.

In China, regulation has been more accommodating allowing players like Ant Financial, valued at $150 billion, to reshape digital payments, loans, and wealth and asset management.

In Europe (including the UK), 20% of the banking and payments institutions are new entrants and have captured nearly 7% of total banking revenue, one-third (33%) of all new revenue since 2005.

The margin compressions and customer churn, across products, means banks have 2 alternatives: either play the volume game or become more sophisticated.

For the volume commoditization game, it means often getting into price wars and fighting to be the most cost efficient through digitalisation.

For the sophistication play, it can be through structuring sophisticated products, or recurring revenue / sticky solutions, or most importantly, being client-centric increasing product density with each client, i.e. at least, cross sell the franchise vs “siloed product pushing”.

The 5 dimensions to look at in the Traditional Banks vs FinTechs battle:

1- Trust: The trust factor towards banks from retail and institutional clients is still very strong. That’s one of the reasons why robot advisors are still struggling to take off. Most clients are still comfortable today to keep their cash and securities in banks. Will it stay so?

2- Data: For example, PSD2 regulation is opening banking data: the smallest fintech provider can get access to elaborate transaction records and use that data in new and interesting ways, if customers provide their approval to do so.

3- Credit is a key angle to attract new clients (retail or institutional). Many new entrants, including Ant Financial, are looking to offer credit to clients.

4- Innovation: Banks are under increased regulatory scrutiny, which suppresses appetite to take innovative risks.

5- Customer experience: For example, Standard Chartered has aligned its cash management offering with WeChat’s online payment gateway, giving corporate merchant customers access to 800 million consumers in China

How can banks cement their relevance with customers and regain revenue growth?

There is no doubt for me that survival of banks comes through keeping and attracting clients through a solid trust factor / customer experience, becoming the gateway like a Apple who owns the relationship, and being able to leverage SaaS “pay-as-you-go” applications in a nimble way, freeing themselves from legacy infrastructures. This is the platform play many industries are going through. AirAsia CEO Tony Fernandes says the future is being a digital travel company, a more open platform that potentially invites in the competition and sells ancillary products.

Tell us more about the platform play?

In the industrial area, it was all about process efficiencies, six-sigma, “waterfall” models, siloed departments. Today we “pay as we go”: a teenager can get you 1 million views on YouTube cheaper than an ad agency, you can get a room without going to a hotel, you can get a ride without being in a taxi.

We are moving from a siloed model to an ecosystem model where we are organised by purpose, from “beating the competition” to “being the competition”, from big idea to big data, from company-centric to client-centric, from ad agency driven to storytelling for customers, from disciplined to creative and innovative employees, from Pipeline to Platform.

Banks are starting to organise multi-disciplinary innovative teams by purpose rather than skills.

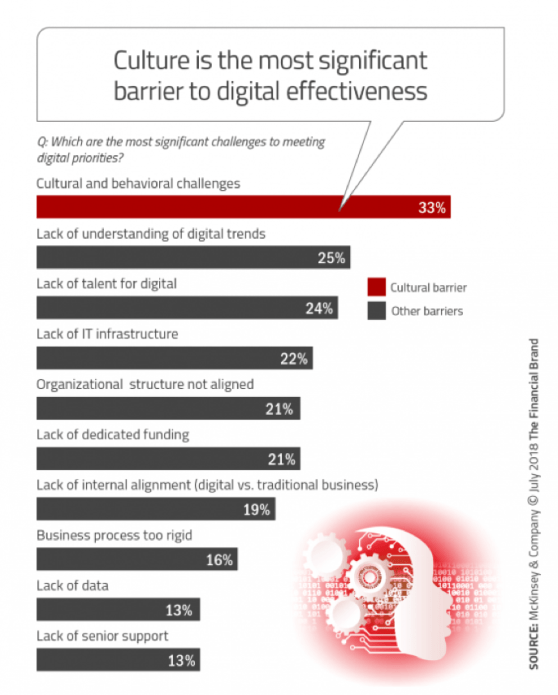

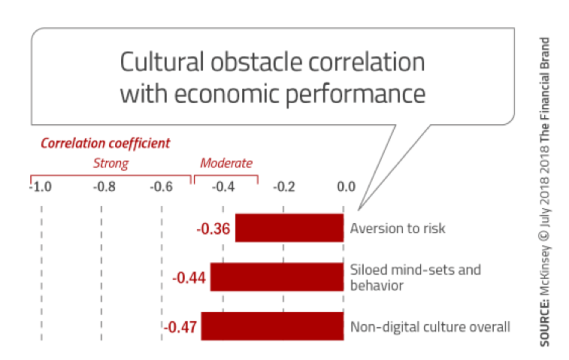

Digital Transformation is more about people than digital. That’s why it takes time. Culture is the biggest barrier to Digital Transformation.

How do banks manage the culture shift?

Shifting traditional mindsets and operating models to deliver digital journeys at a start-up pace is no easy feat for a financial giant.

From a McKinsey study, the 3 main culture barriers are:

1. the presence of functional and departmental silos,

2. a fear of taking risks,

3. the difficulty of forming and acting on a single view of the consumer.

Two opposite forces are pulling banks: the constant and increased compliance scrutiny and the need to innovate.

How do you let the crazy Doc from “back in the future” thrive in a top investment bank? How do you nurture and reward this innovative DNA? Organic culture shift will be too slow.

How do you keep the pace of innovation and agility to change when you have a big ship to steer? Acquisition of start-ups? Sandbox experiments?

Some banks are creating sandbox Neo-Banks. DBS created its digibank in India. Some banks may become the new Kodak, failing to move in the digital age.

Engineer Steven Sasson was turned down by Kodak’s management when he showed them the digital camera, due to fears of cannibalization. Either you wait for competition to put you out of business or you become it.

Also, do you push a product or truly solve a pain point? Starbucks wants to be your third place after your home and office. You can get cheaper coffee elsewhere. What they are truly selling to you is space, i.e. going beyond siloed coffee product pushing, solving directly the pain point.

Again, Digital Transformation is more about people than digital. It requires a big cultural shake up. Let’s follow Einstein and his “Creativity is the intelligence having fun”.

Juggling between a finance career and start-ups is quite unusual!?

Social status today is conditioned mostly by your professional occupation, which is indicative of a whole range of identity markers: income bracket, level of training, belonging to a social “class” and all the supposed cultural habits that go with it. Slashing is challenging this view, i.e. focusing more on skills and eagerness to grow vs status. Slashing refers to the slash sign, as in “/”, and refers to people who combine more than one role or occupational identity, juggling with cultural codes as well as professional identities.

I enjoy the intensity and intellectual stimulation of working quadruple shifts and heavily action-driven (intense focus on one project at a time). I am extremely grateful to be surrounded by great teams on each project.

I feel passionate about creating, in start-ups as well as banks.

How many start-ups are you involved in?

I have been involved with 8 start-ups at different levels of involvement. I co-founded most. I never start a business on my own.

My number one criteria: I invest my energy in people I believe in, mostly their appetite to get things done. We feed each other from our mutual energy and vision. I tend to prefer start-ups based on service (lower fixed costs), with a human and tech angle. For example:

– PixiumDigital: software development from app dev, website dev, IoT, data analytics, VR, to interactive display..

– KidsCampSingapore: founded 4 years ago, with thousands of kids coming, I am very proud that it has been voted best kidscamp in Singapore for the second year in a row by SassyMama. And, even for Kidscamp, we are undergoing a digital transformation of our back to front end.

– GoMasterCoach: For life coaches: 1/ a school to get their certification, 2/ online classes and 3/ a webapp: toolbox with all the tests/programs life coaches need.

What keeps you going is the satisfaction of creation, the intellectual stimulation as well as the collaboration with talented individuals.

How “Dare you” to be a serial woman entrepreneur in tech?

Good question. First time I ran a triathlon, one of my female friends asked me what was my time target for the triathlon. I answered “3 hours”. She very candidly replied “how dare you think you will do as good as our guy friends!”.

I value being a woman but it doesn’t define me or gives me any limit. You set your own limitations. Your beliefs define you.

Like for a triathlon, you have to dare believing in yourself, learn from your ability to adapt and make sure you have insane discipline to deliver.

How do you bring more diversity?

I was heading women networks in the different banks I was with. How do you break the “boys club”? How do you make sure women who “join the club” keep their diverse mindset and don’t mimic men? How do you prevent women from pursuing an individual strategy of advancement that centers on distancing themselves from other women?

Unfortunately, I am convinced the ‘Diversity & Inclusion’ initiatives have to be very top driven, such as the “Council for Board Diversity” in Singapore or the “30% Club”: campaigning for more women on boards, preparing them to be board-ready, giving scholarships, promoting cross-organisation mentoring or providing leadership courses.

At a more junior level, I always try to proactively go to women to suggest a role. I often get “I am not ready. I need extra experience.” Mentoring is more often on self-confidence than capability.

We are missing half the talents if they get demotivated by this closed club.

Singapore listed companies had 7% women on their boards 5 years ago. The target is 20% by 2021.

Aurelie, thank you !

Get in touch with us @ womenfrenchtech at gmail dot com

In collaboration with Amel Rigneau & Sophie Guo